MEMORANDUM

TO: Clients and Friends of Ariel Investments

FROM: John W. Rogers, Jr., Chairman and Co-CEO

Mellody Hobson, Co-CEO and President

DATE: June 17, 2024

RE: Happy Birthday, EMV!

Past performance is not indicative of future results. An investment’s return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data as of the most recent month-end may be obtained by visiting our website, arielinvestments.com.

It has been one year since we enthusiastically announced the launch of Ariel Emerging Markets Value (EMV) under the leadership of Henry Mallari-D’Auria, who has exceeded all expectations. Henry joined us after a successful 31-year career at AllianceBernstein (AB)—a tenure that included serving as Chief Investment Officer of Emerging Markets Value Equities with a near decade-long overlapping role as Co-Chief Investment Officer of International Value Equities. In recognition of his exceptional leadership right out of the gate, Henry was named Executive Vice President at year-end—a title held by only three other senior Ariel leaders.

An emerging markets value strategy was a natural product extension for Ariel. Like our domestic equity strategies which focus on smaller companies, our EMV portfolios also target securities that are less widely followed and therefore more likely to be inefficiently priced. Henry’s well-honed, bottom-up research effort embraces the active patience that we believe is needed to drive long-term returns.

Henry initially launched Ariel Emerging Markets Value and Ariel Emerging Markets Value ex-China with four long-tenured AB colleagues who joined our firm because of their desire to remain together. Each is impressive and fits right into our team culture. They are:

Vlad Byalik, Portfolio Manager and Senior Research Analyst

- 19 years at AB | 27 years of experience

- MBA, Wharton School of Business | BA in Economics, Wesleyan University

- Fluent in Russian

Christine Phillpotts, CFA®, Portfolio Manager and Senior Research Analyst

- 10 years at AB | 19 years of experience

- MBA, Harvard Business School | BA in Economics, Columbia University

- Fluent in French

Slava Breusov, Senior Research Analyst

- 10 years at AB | 23 years of experience

- MBA, Wharton School of Business | Degree in Economics, Siberian Academy of Public Administration

- Fluent in Russian

Ted Mann, CFA®, Senior Research Analyst

- 16 years at AB | 19 years of experience

- BS, Duke University

- Fluent in French

In recent weeks, another AB colleague, Vivian Lubrano, joined Henry to work as a portfolio manager alongside Micky Jagirdar on our international/global portfolios, which speaks volumes about Henry’s reputation.

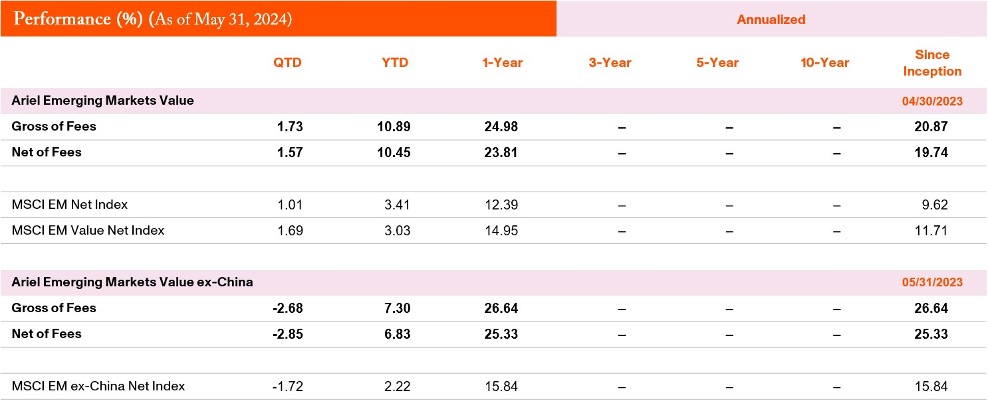

In many respects, our timing for launching a new emerging markets strategy could not have been better. Values were abundant—and continue to be—as investors remain skeptical of EM when viewed through the lens of comparatively booming developed market economies. And while Henry and the Ariel EMV team have been hunting for value with a catalyst, they have uncovered some compelling investments that have allowed them to significantly outperform their benchmarks.

To that end, we thought it noteworthy to share the recent eVestment rankings (as reported on June 12, 2024). As evidenced by the excellent returns for the one-year periods, we believe Henry’s process is clearly working.

Given our long-term approach to investing, we would never want to overstate the importance of one-year results. That said, we are pleased to have our newest EMV strategies launch with favorable relative returns—underscoring the benefits of taking a contrarian view and playing the long game. Henry has been managing EMV strategies since 2001 and we are excited to have his expertise along with his long-tenured team at our firm. His first year at Ariel is only the beginning. We believe his commitment to excellence will benefit our investors for years to come.

As always, feel free to contact us if you have any questions or need additional information.

*Ranking data is as reflected on the eVestment database as of the date the data was downloaded. eVestment may change this data subsequently without notice due to their receipt of updated or changed information. Ariel may not become aware of any such change and does not have a duty to report any such change subsequent to the issuance of this letter. eVestment listed Ariel Emerging Markets Value Composite in the Global Emerging Markets All Cap Value Equity and Ariel Emerging Markets Value ex-China Composite in its Emerging Markets ex-China Equity rankings. Criteria are a minimum of one year of performance history, updated portfolio characteristics, and country/current allocations disclosure, respectively. Ariel did not compensate eVestment to participate in this ranking. More detailed information regarding the survey methodology and tabulation of results can be found at https://www.nasdaq.com/solutions/evestment. Ratings, rankings and awards do not imply that Ariel will or has been successful in its product and strategy offerings or services, and they may not be indicative of Ariel’s investment performance or any future investment performance or sustainability accomplishments. The rating, ranking or award may not be representative of any client’s individual experience.

Investments in non-U.S. securities may underperform and may be more volatile than comparable U.S. stocks because of the risks involving non-U.S. economies, markets, political systems, regulatory standards, currencies, and taxes.

The use of currency derivatives, exchange-traded funds (ETFs), and other hedges may increase investment losses and expenses and create more volatility. Investments in emerging markets present additional risks, such as difficulties in selling on a timely basis and at an acceptable price. The intrinsic value of the stocks in which the portfolios invest may never be recognized by the broader market. The portfolios are often concentrated in fewer sectors than their benchmarks, and their performance may suffer if these sectors underperform the overall stock market. Investing in equity stocks is risky and subject to the volatility of the markets.

Past performance does not guarantee future results. Performance results are net of transaction costs and reflect the reinvestment of dividends and other earnings. Net performance of each Composite has been reduced by the amount of the highest fee charged to any client in each Composite during the performance period. Actual fees may vary depending on, among other things, the applicable fee schedule and portfolio size. A complete fee schedule is available upon request and may also be found in Ariel Investments LLC’s Form ADV, Part 2. Returns are expressed in U.S. dollars. Current performance may be lower or higher than the performance data quoted.

The opinions expressed are current as of the date of this commentary but are subject to change. The information provided in this commentary does not provide information reasonably sufficient upon which to base an investment decision and should not be considered a recommendation to purchase or sell any particular security. There is no guarantee that any expressed views will come to fruition or any investment will perform as described.

Investors cannot invest directly in an index. The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 1,377 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country. Inception of this benchmark was January 1, 2001.

The MSCI Ariel Emerging Markets Value Index captures large and mid-cap securities exhibiting overall value style characteristics across 24 Emerging Markets (EM) countries. The value investment style characteristics for index construction are defined using three variables: book value to price, 12-month forward earnings to price and dividend yield. Inception of this benchmark was December 8, 1997. MSCI Emerging Markets ex-China Index captures large and mid cap representation across 23 of the 24 Emerging Markets (EM) countries excluding China. Its inception date is March 9, 2017.

All MSCI Index net returns reflect the reinvestment of income and other earnings, including the dividends net of the maximum withholding tax applicable to non-resident institutional investors that do not benefit from double taxation treaties. MSCI uses the maximum tax rate applicable to institutional investors, as determined by the company’s country of incorporation. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used to create indices or financial products. This report is not approved or produced by MSCI.